The Association for Investment Management and Research, a world-wide, though North American dominated, organization of financial analysts, which became "The CFA Institute" in 2004.

A constant of passwordAccessType used within the user authentication and administration processes (e.g. editUserBox) to determine the user's authorization to use various features of HIMIPref™.

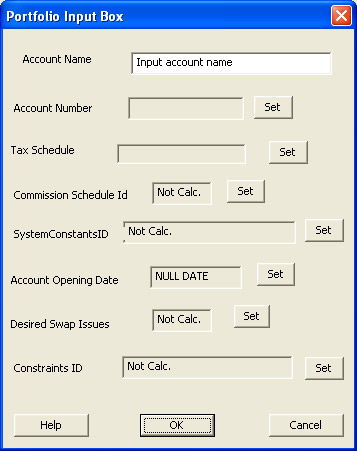

A field contained in a portfolioDataRecord which specifies the legal name of the account's owner. This is used in the preparation of reports, confirmations, etc. Any characters are allowable for input, up to a limit of ACCOUNT_NAME_LENGTH characters.

When individual securities are assigned an account (e.g. in the preparation of a performanceReport), the "accountName" is the longName of the instrument.

A field in the portfolioDataRecord which uniquely identifies a separate account - which may be an actual client account or a notional account used for research purposes. An "accountNumber" will have ACCOUNT_NUMBER_LENGTH characters.

Also a field in a holdingsDataRecord, serving to identify the portfolio owning the position signified by the record.

When individual securities are assigned an internal "accountNumber" (e.g. in the preparation of a performanceReport), these account numbers are "XX" followed by the securityCodes of the instruments.

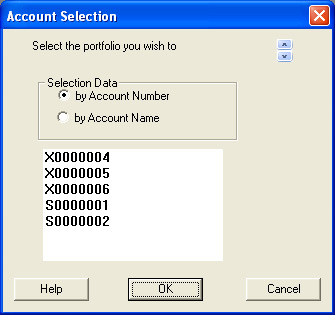

An input box which allows selection from any of the accounts listed in the portfolio table.

To select an account, simply highlight the desired element of the displayed list and click the "OK" button. To select no account, click the "Cancel" button.

The list of accounts can be formatted according to either accountName or accountNumber in accordance with the radio-button selected under the heading "Selection Data".

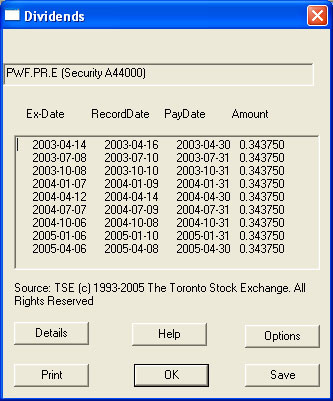

Dividends on preferred shares (and interest on preferred securities) do not accrue on a daily basis - the income is simply paid if, as and when declared. Never-the-less, there is sufficient regularity and certainty of these payments that the market price of these securities may be expected to follow a sawtooth pattern - the price rising until the ex-date and falling immediately to reflect the amount of income which has just become payable to the holders.

Hence, a calculation of "accrued dividends" can have some relevence, with the objective of stripping this effect from the quoted price to arrive at, for instance, the Current Bid (FlatValue)

The calculation proceeds with the following steps:

The dividend record with the ex-date immediately prior to the calculation date is obtained

The dividend record with the ex-date immediately following the calculation date is obtained (by estimation, if necessary)

The pay-date corresponding to the prior ex-date is then obtained

The "accrued dividend" is then the amount of the next dividend, times the fraction of the period elapsed from the prior payDate.

Note that this value for "accrued dividends" may be negative, if the calculation date is prior to the payDate of the dividend record corresponding to the immediately prior ex-date.

The portfolio currently being examined by HIMIPref™. This may be changed via the "Set Portfolio as Active" selection on the portfolioListReportContextMenu|accountName context menu.

This term is applied to those issues which have a dividend rate that is adjustable by the issuer in a manner that does not lend itself to analysis by HIMIPref™. For example, the issue of Epcor Preferred Equity Inc. Cumulative Redeemable First Preferred Shares, Series 1 has terms defined in the prospectus whereby after October 1, 2007, the floatingRate option is dependent upon the five-year Government of Canada Yield. This is the only issue examined which has such terms - similar instruments are amenable to analysis as the floatingRate option is dependent upon the Canada Prime Rate and there exists a sufficient number of these instruments to form a homogeneous group upon which historical behaviour may be tested. Thus, "adjustableRate" preferred shares are marked with the PRICING_EXCLUDED_ADJUSTABLERATE flag in the pricingCode field of their instrumentDataRecord - at least until such time as sufficient data is available to allow some confidence in the results of historical analysis.

The adjusted cost base of a security position is the net amount of money paid to hold it and is usually reported on a per-share basis. When securities are held long only, then purchase amounts are added to the adjusted cost base and may change the per-share value, while when shares are sold they are each assumed to have cost an amount equal to the then-current adjusted cost base and a capital gain or loss reported on the difference between this figure and the actual receipt.

If the issue bought has a risk attribute for which the issuer concentration is controlled, the trade is examined to determine whether the purchase will result in the total weight of that issuer in the portfolio exceeding the value of the control. If so, the size of the trade is reduced accordingly.

In the issue method, if the parameter is set to a valid non-zero value, then the parameter will be raised, if necessary, to the inverse of the numberSwapSecuritiesDesired : that is, if the parameter is set to 1%, but only two securities are desired to be held, then the calculation will be performed with a maximum weight for that issuer of 50%.

This procedure is called by adjustForSectoralMaxWeights in the determination of trade size. It is called with a particular yield curverisk attribute - e.g., whether it is a retractible and/or floating rate issue. If this risk attribute is different for the issues bought and sold and the maximum/minimum weight of that component in the portfolio is defined, the weight of that component in the portfolio is determined. If the maximum/minimum weight of that attribute in the portfolio will be exceeded/undershot through execution of the trade, the trade size is reduced accordingly.

In the issue method, if the parameter is set to a valid non-zero value, then the parameter will be raised, if necessary, to the inverse of the numberSwapSecuritiesDesired : that is, if the "constraint parameter" is set to 1%, but only two securities are desired to be held, then the calculation will be performed with a maximum weight for that sector of 50%.

Components which are constrained and their constraint parameters are:

A procedure called during the calculation of trade size.

This procedure examines the weight of the purchased issue after execution of the putative trade. If this weight is less than effectiveMinWeight, the size of both the purchase and sale are reset to 0.

This is a fairly technical adjustment, called to ensure that rounding errors are not propogated to the solution. If the number of shares purchased is zero, the number sold is non-zero and there is a positive cash balance in the account, then the number of shares sold is re-set to zero.

A procedure called by calculateTradeSize during the calculation of tradeSize to ensure that indicated trades are reasonable in light of historical trading volumes.

If the product of maxDaysToTrade and volume - average is less than the size of the indicated trade (for either the purchase or sale), then the trade size is reduced accordingly.

A procedure called during the calculation of trade size.

If the sale indicated by the trade would leave the sold position with a weight in the portfolio of less than PARAMETER_PORTFOLIO_MINWEIGHT, then the sell size is adjusted upwards to sell the entire position.

The amount left to the investor after payment of taxes: if a dividend payment is $1.00 and the investor's marginalTaxRate for dividends is 32.9%, the after-tax value of the dividend is $0.671.

A field in an instrumentDataRecord that specifies the annual dividend that is to be paid on the instrument in accordance with the prospectus. In the case of floatingRateInstruments, this value is set to zero and equivalent calculations performed as necessary in accordance with information recorded in the instrument's instrumentFloatingRateDataRecord. In the case of fixedFloaters, the value is that of the fixed rate payable.

A scaling factor used in the calculation of rewardComponentsBid / rewardComponentsAsk to ensure that individual raw analytical values are treated as annual percentages, a convention utilized to

Ensure that there is some degree of physical meaning to the valuation, rather than these values being reported on an arbitrary scale, and

to ensure that there is only one set of optimized optimizable parameters, rather than an infinite set of values maintaining the same proportions.

(i) The "ask" represents the price at which at least 100 shares (a board lot) may be bought. Simulation methodology assumes that the value of shares which may be purchased at the day's closing "ask" is equal to the tradeable value of the issue.

The "ask" reported by the system and used in simulations is derived from exchange data according to the following methodology:

if the exchange reported an actual non-zero closing ask, then this value is used.

if the exchange did not report a ask, but reported a closing bid greater than $1, then the value used is $1 more than the bid.

if the exchange reported neither a bid nor an ask for the security at the close of business, then the value used is $0.50 more than the most recent close of the security.

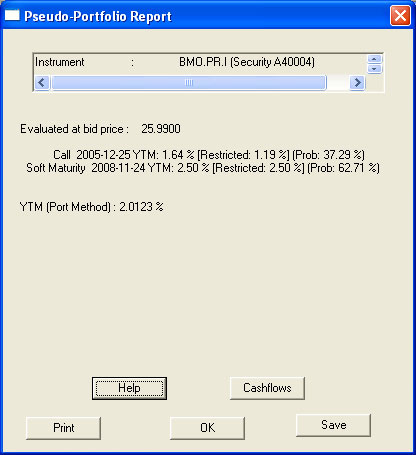

The yieldToMaturity of the element of the optionCalculationList that is the lowest (scenarios which involve the exercise of retraction privileges excepted), when the calculations have been performed using the ask price.

This is the mean average price under a normal distribution centered at the expectedBid, considering only that area of the curve for which the cumulative probability is greater than that indicated by the probable exercise of prior puts and less than that indicated by the probable exercise of prior calls.

In this calculation, the normal distribution is divided into 101 segments, each with a width of 0.05 standard deviations, where the standard deviation is set as being the period volatility. Each segment is then examined - if the segment is sufficiently high (in terms of cumulative probability) to assume that a prior put (or sufficiently low, for prior calls) has not been exercised, the midpoint of the segment is assumed to be the price of the entire segment and this price incorporated into the average weighted by the probability of the segment.

Note that this calculation implicitly makes the assumption that the deviation of market valuations from the expected value are monotonic - a Monte Carlo calculation has been deemed unnecessarily complex for analytical purposes.

A calculated value used in the cost method of option pricing and provides an indication of what the price of an instrument could be expected to be if an embedded option that is considered to be exercised were not to have been exercised - for example, if an issue were to have two equally possible prices, $24.50 and $25.50 and a retraction option exists with an exercise price of $25.00, we might then consider that the retraction will be exercised if the lower price would otherwise be effective (and not otherwise) and the "average price if exercised" will be $24.50.

The Bank of Canada is Canada's central bank, with responsibilities focussing on the goals of low and stable inflation, a safe and secure currency, financial stability and the efficient management of government funds and public debt. Further information is available on its website.

A "bankruptcy" occurs when a corporation is no longer able to meet its obligations and the creditors of the firm (including corporate financers, such as holders of preferred shares, in accordance with the terms of the prospectus) liquidate the firm's assets (or recapitalize the company) and make what recovery they can from the realized value. This is the most extreme example of a reorganization

A dialog box accessible via any of the selections on the tradeMenu|Reports|BestTrades popup menu. It displays the best trades for which tradeFeasible is true referenced on the tradeReport, sorted as indicated by the actual selection. The user may specify the number of trades to be ranked on this report by clicking the "Set List Length" button.

(i) The bid represents the price at which at least 100 shares (a board lot) may be sold. Simulation methodology assumes that the value of shares which may be sold at the day's closing bid is equal to the tradeable value of the issue.

The bid reported by the system and used in simulations is derived from exchange data according to the following methodology:

if the exchange reported an actual non-zero closing bid, then this value is used.

if the exchange did not report a bid, but reported a closing ask greater than $1, then the value used is $1 less than the ask.

if the exchange reported neither a bid nor an ask for the security at the close of business, then the value used is $0.50 less than the most recent closing trade price of the security.

A calculated value, used in the calculation of tradeDesirability and tradeScore, calculated by comparing the valuations of the two instruments involved in the trade, valuing the instrument to be sold at the bid and the instrument to be purchased at the offer

The yieldToMaturity of the element of the optionCalculationList that is the lowest (scenarios which involve the exercise of retraction privileges excepted), when the calculations have been performed using the bid price.

A portfolio defined by the system when, for one reason or another (usually the unavailability of pricing information for an issue presumed to be held by the previously activePortfolio) computations are not otherwise feasible.

The "blankPortfolio" is initialized with the following values in its portfolioDataRecord:

A standardized number of shares, set by the relevent Exchange as part of their rules. On the Toronto Stock Exchange, it is defined as

A trading unit of shares. The board lot size of a security is determined by the previous day's close price. Close less than 10 cents: 1000 shares board lot. Close between 10 cents and $1.00: 500 shares board lot. Close $1.00 or higher: 100 shares board lot

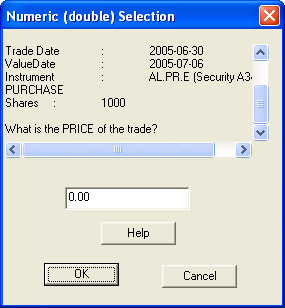

An input box that allows the user to answer the indicated question by clicking on either the "Yes" or "No" button.

Note that the captions of the buttons may vary by context; e.g., they will be labelled "Sale" and "Purchase" when the indicated question is "Is this trade a SALE?".

A calculated value used in the subsequent calculations of bidToOfferPickup. It is defined as

buyValuationAsk = totalRewardAsk [of the instrument bought]

This value seeks to give a single number reflecting the attractiveness of the instrument being bought at its ask price before accounting either for the portfolio's holdings of the security in question or for penaltyComponents .

CFA Charters are issued by AIMR. CFA stands for "Chartered Financial Analyst". The charter is awarded after the successful completion of three annual examinations (which are prepared for through home study) and relevent experience in the financial industry. The CFA Charter is usually regarded as being roughly equivalent to an MBA with a specialization in finance.

In the case of 1:1 conversion, this will be equal to the calculatedSellPrice; when the conversion ratio is not 1:1, the "calculatedBuyPrice" will be adjusted so that the total book value of the position is unchanged.

A calculated value based on the number of shares and the values stored on the appropriate commissionDataRecord. This number provides the total commission payable on a trade of the supplied number of shares and is calculated as:

In the issue method, when the parameter numberSwapSecuritiesDesired is 0 (i.e., the calculation is being performed for theoretical purposes), the result is 1.0 + the weight of the issue currently held.

The term "trade size" is shorthand for its two components: sellSize and buySize.

Note that some of the constraints limiting the proportion of investment in a particular sector may be over-ridden by the inverse of desiredSwapIssues if this value is defined.

A type of option which gives the holder the right, but not the obligation, to buy securities at a specified price at a specified time in the future. In the preferred share universe, most issues will have "calls" as embedded options, with the issuer having the right of exercise. An issue for which a "call" exists is referred to as "callable".

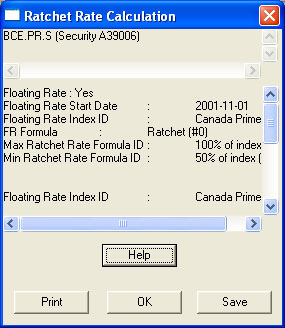

the average ... of the annual rates of interest announced from time to time by the [Canadian Schedule A] Banks as the reference rates then in effect for such day for determining interest rates on Canadian dollar commercial loans made to prime commercial borrowers in Canada

(the language has been taken from the prospectus for the Northern Telecom Limited Non-cumulative Redeemable Class A Preferred Shares Series 7, which currently (December, 2003) trade on the Toronto Stock Exchange as NTL.PR.G.

This rate is also defined and compiled by the Bank of Canada and reported on its website.

Securities regulation in Canada falls within the jurisdiction of the provinces or territories, rather than being a federal matter. As such, each province or territory has its own securities regulator. The Canadian Securities Administrators (CSA) is an "umbrella" organization, which is comprised of all provincial and territorial securities regulators and provides in essence, a "virtual" national securities regulator. One of the activities of the CSA is to provide investor education materials for distribution by member regulators.

One of the activities of the CSA is the maintenance of SEDAR.

A capital gain results when the net proceeds from a security sale (after directly related expenses) exceeds its adjusted cost base. Due to differing marginal tax rates, capital gains are generally the most desireable type of income to have.

Cash held in a demand account at a financial institution, or currency, or a financial instrument issued by a financially strong institution with a very short term and great liquidity in the market-place, so that it may readily be turned into an amount of cash known with great precision. An example would be Government of Canada Treasury bills with a term-to-maturity of three months or less.

This value, when used specifically to refer to the cash position of a portfolio, is displayed by the portfolioReportBox.

The total "cash and equivalents" holding of a portfolio tracked in detail by HIMIPref™ may be viewed on the transactionReport and is reported on the portfolioListReport.

A flowType which indicates that the parent cashFlowEntry has been created to represent an adjustment to the first dividend payment, which will have been processed as CASHFLOW_DIVIDEND at the standard rate, but which may actually have a non-standard cashFlowAmount in accordance with the terms of the prospectus.

A flowType which indicates that the parent cashFlowEntry has been created to represent the last dividend payment of the series, which may therefore have a different cashFlowAmount than other elements of the series and a cashFlowDate not evenly spaced with the other elements.

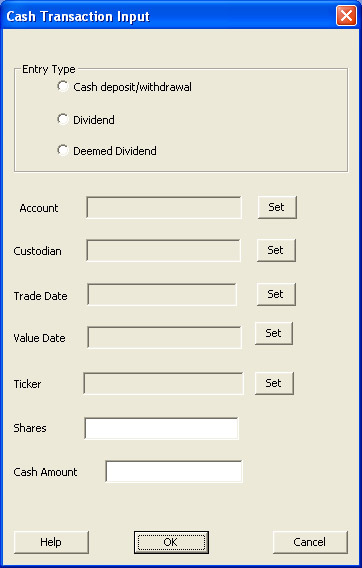

A dialog box accessible via the "Process Cash Entry" command of the mainMenu|Admin popup menu, which allows for the creation of a transactionDataRecord reflecting the following user inputs:

A term used to refer to the value of a particular holding in a portfolio. It is equal to the product of the two applicable fields on the holdingsDataRecord: if holdings is positive, it is holdings * bid; otherwise, it is holdings * ask.

Membership in this parameterClassType indicates that the parameter is representable by a real number (as opposed to an integral or character-based flag).

This scaling factor is calculated as the inverse of the sum of all parameters in this class - therefore, when the parameters in this class are multiplied by the scaling factor and then summed, the total is 1.0. This is a useful property when considering classRewardYieldBid / classRewardYieldAsk as this value will be the percentage expected return on the instrument as determined by a blended estimate of the yield of the instrument.

This class of parameters indicates that its members are optimizableParameters, and that a simulation involving a change to one or more of them will run relatively quickly as neither universeAverages nor instrumentAveragesRecord must be recalculated.

This class of parameters indicates that its members are optimizableParameters, but that a simulation involving a change to one or more of them will run relatively slowly as either universeAverages or instrumentAveragesRecord must be recalculated.

This class of optimizableParameters is designated for cosmetic purposes only. It indicates that the parameters so described, listed under the heading "PORTFOLIO PARAMETERS" in the analyticalParametersReportBox, are used to describe attributes of the specific portfolio for which the valuation is made, rather than reflecting intrinsic characteristics of the preferred share universe.

If the parameter is a member of the class CLASS_PARAMETER_CURVEAVERAGING and is a member of the class "CLASS_PARAMETER_REVERSION", it is reported under the heading "CURVE REVERSION PARAMETERS"

If the parameter is a member of the class CLASS_PARAMETER_INSTRUMENT_VALUATION and is a member of the class "CLASS_PARAMETER_REVERSION", it is reported under the heading "INSTRUMENT AVERAGING PARAMETERS [Reversion]"

If the parameter is a member of the class CLASS_PARAMETER_INSTRUMENTAVERAGING but not a member of the class "CLASS_PARAMETER_REVERSION", it is reported under the heading "INSTRUMENT AVERAGING PARAMETERS [Calculation]"

This class of parameters is designated for cosmetic purposes only. It indicates that the parameters so described, listed under the heading "SYSTEM PARAMETERS" in the analyticalParametersReportBox are best described as being fundamental constants used in the course of calculations throughout HIMIPref™. However, provision has been made for varying these parameters on an occasional basis.

This class of optimizableParameters is designated for cosmetic purposes only. It indicates that the parameters so described, listed under the heading "TRADING PARAMETERS" in the analyticalParametersReportBox have no effect on valuation, they are used in the process of trade determination only.

(i) The price of the last trade executed on the exchange on the day in question.

(ii) A field in a priceDataRecord recording the "close" according to the exchange for the specified securityCode and date. This datum is not routinely gathered - it is recorded only when the security has no bid and no ask reported.

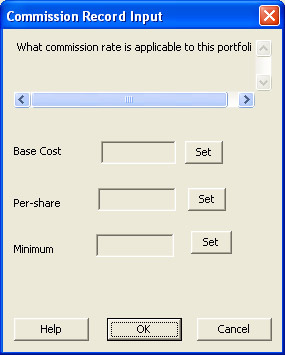

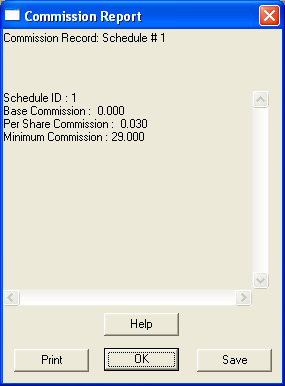

The basic charge for executing a trade, irrespective of quantity. For example, while a broker may charge institutional clients five cents per share, regardless of size, the custodian may charge $20 for every settlement, regardless of size. This $20 fee would be the "commission base" when preparing the commission data record.

This field specifies the minimum commission payable in order to execute a trade. For example, discount brokers in Canada may charge three cents per share on trades, with a minimum of $29.00.

This field specifies an identifier for the record which may be used by other data records to refer to the commission record. Other records which key on this value include:

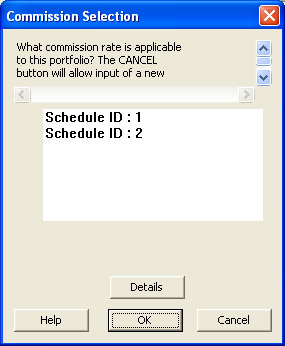

A dialog box accessible via the portfolioInputBox, which allows the selection of the commissionScheduleID applicable to the portfolio being defined. A central list box allows the highlighting of a single commissionScheduleID; clicking

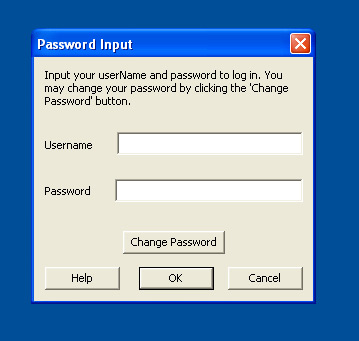

A field in the editUserBox and passwordChangeBox that requires the user to retype the string input into the password field in order to confirm that there have been no typographical errors in the input.

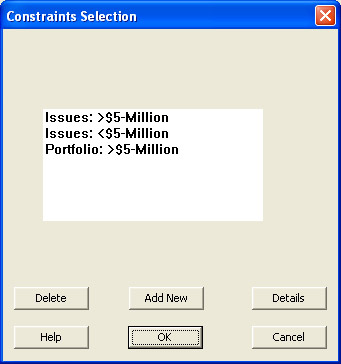

A constraint is an arbitrary constant imposed upon the system. While investigations may take place from time to time to check the reasonableness of the values, they are not considered to be optimizable parameters. Constraints are:

The description field of all constraintSpecificationRecords is displayed in a normal list box. The following operations may be performed through clicking the appropriate buttons:

Delete : attempts to delete the highlighted record. If this record is required as it is specified in an extant portfolioDataRecord, no action will be taken.

Add New : displays the constraintsInputBox for the creation of a new record.

This is an acronym for "Canadian Originated Preferred Securities", a term trademarked by Merrill Lynch to denote Preferred Securities. Such instruments pay interest income.

The "costAskDiscountingTable" is used for the determination of cost yield at the ask price and as the base for the curveAskTable. The cash flow entries in this table are computed in the following order:

The "costBidDiscountingTable" is used for the determination of cost yield at the bid price and as the base for the curveBidTable. The cash flow entries in this table are computed in the following order:

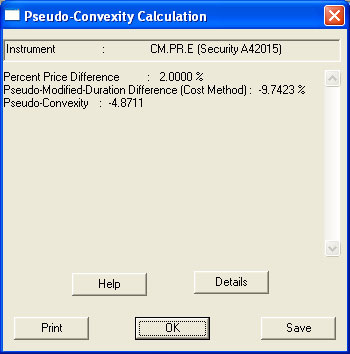

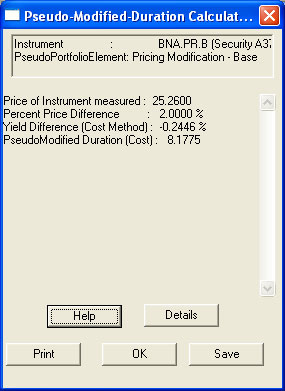

A calculated vector of (PSEUDO_PORTFOLIO_INDEX_MEMBERS-2) entries, used in subsequent calculations of pseudoModifiedDurationCost. It represents the differences in costBidYield between all but the highest and lowest priced elements of the pseudoList relative to their flanking members, so that the "costBidYieldDifference" corresponding to pseudoList[i] is

A technique of valuing embedded options which is the foundation for the cost method of instrument valuation.

Once the basic option calculation list has been calculated, each component of that list is assigned a value in accordance with the "cost method of option pricing" and this value incorporated into the projected cash flows of the instrument's costBidDiscountingTable and costAskDiscountingTable.

The complete set of options available to the issuer and the investor is considered and a value assigned to each option. These option values are incorporated into an over-all yield evaluation. Very similar to curve yield but uses the cost method of option pricing. See costBidDiscountingTable for details of the calculation.

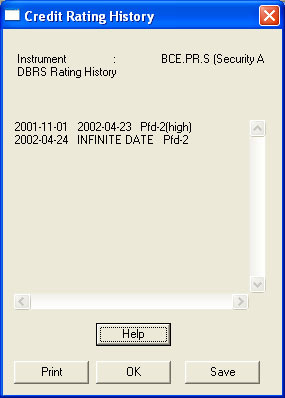

Credit classes are used to quantify the creditworthiness of the various issuers who are considered in the investment universe. It should be noted that the determination of a credit rating on an issue is entirely independent of its price: the sole focus is on whether the issuer will be able to meet the terms listed in the prospectus. There are several companies who are engaged exclusively in the field of credit analysis, an example being DBRS. The credit classes considered in HIMIPref™ are credit Class 1, credit class 2 and credit class 3, as modified by the adjustments credit class high and credit class low. Issuers insufficiently credit-worthy of even the lowest rung, Credit Class 3 Low, are considered to be unrated for analytical purposes and are not eligible for investment consideration in HIMIPref™. See the procedure eligibleForPurchase.

Information regarding "creditClass" ratings for each instrument is contained in the creditRatings table of the permanentDatabase.

The highest of the three major credit classes, Credit Class 1 is reserved for those issuers for which will almost certainly be able to meet the obligations they shouldered under the terms of the prospectus for the issues under consideration. Most issuers in this class are banks or other financial institutions. HIMIPref™ relies primarily upon the credit ratings assigned by DBRS to assign issues to the credit classes. Credit Class 1 may be considered a risk attribute by construction, since if the issue is considered to be investible and is neither of credit classes 2 or 3, it is Credit Class 1 by default.

Information regarding "creditClass" ratings for each instrument is contained in the creditRatings table of the permanentDatabase.

The lowest of the three major credit classes that are eligible for consideration for investment in HIMIPref™, Credit Class 3 is for those issuers which should be able to meet the obligations they shouldered under the terms of the prospectus for the issues under consideration, but which may experience difficulties in bad economic times. HIMIPref™ relies primarily upon the credit ratings assigned by DBRS to assign issues to the credit classes. Credit Class 3 is considered a risk attribute.

Information regarding "creditClass" ratings for each instrument is contained in the creditRatings table of the permanentDatabase.

When this datum is reported as a number, {0 is false; 1 is true}.

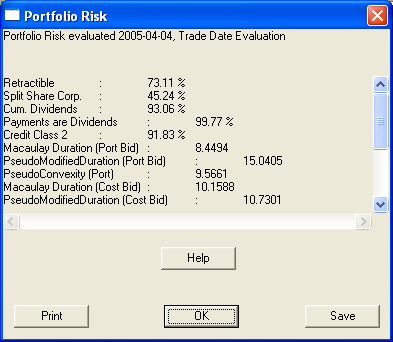

A weighted average for a portfolio for this attribute is reported by the portfolioRiskReportBox.

Something of a misnomer, since most issues characterized as belonging to this creditClass are, in fact, rated, but are not sufficiently highly rated to belong to creditClass1, creditClass2 or creditClass3.

A company established to examine the financial status of debt issuers and form a judgement as to the likelihood of these issuers being able to meet their obligations in a timely manner. The issuers are charged a fee for these judgements and the "creditRatingAgency" makes its views known to potential investors.

Current "creditRatingAgencies" in Canada include CBRS and DBRS.

A record contained in the creditRatings table of the permanentDatabase. This table allows the determination of the effective creditRatings of each preferred share in the universe as of any date analyzed by HIMIPref™.

(i) Credit ratings are assigned by companies such as DBRS to issues. They seek to measure the likelihood of the issuer being able to live up to the terms of the prospectus and do not seek to take a view as to whether the investment is attractive at any particular price. Note that different issues of stock from the same issuer may have different credit ratings based on the degree of protection set forth in the prospectus.

"With the dividend". The entitlement to the dividend in question has not been separated from the ownership of the shares. This separation occurs on the ex-Date.

Dividends are cumulative if they remain owing to investors in preferred shares when not declared in accordance with the schedule specified in the prospectus. There will generally be some constraints placed on the issuer's use of cash (e.g., for common stock dividends) until these arrears are paid. The question of whether an issues dividends are cumulative or not is considered a risk attribute.

This data is recorded in the "cumulativeDividends" field of an instrumentDataRecord.

When this datum is reported as a number, {0 is false, 1 is true}.

if the instrument is normally subject to the influence of the component, the curveMeanPrice is recalculated with the influence removed, and the relevent "curvePriceComponent" set to be equal to the difference. If the instrument is not normally subject to the influence of the component, the "curvePriceComponent" is set to zero.

"curvePriceComponents" for all issues may be displayed on the reportSummary via the "Curve Components (value)" choice on the reportSummary|QuickReports menu.

"curvePriceComponentsProportions" for all issues may be displayed on the reportSummary via the "Curve Components (Fraction)" choice on the reportSummary|QuickReports menu.

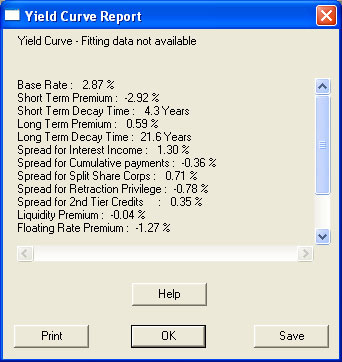

Thus, this set of parameters attempts to quantify the effect on instrument price that will be experienced as the yield curve changes in its predicted manner.

"Curve reversion parameters" may be either positive or negative; a negative value implies reversion-to-mean is operative, while a positive value indicates that momentum is more important.

This is an optimizableParameter. There is no constraint on its size or sign. A negative value implies reversion-to-mean is operative, while a positive value indicates that momentum is more important.

The American Bankers Association's "Committee on Uniform Security Identification Procedures" which, among other things, is responsible for assigning a unique identifier ("CUSIP Number", often shortened to "CUSIP") to any publicly traded security upon request. For further information, see their website at www.cusip.com.

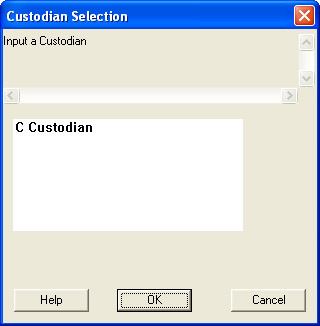

(i) A field contained within a custodiansDataRecord providing a unique identifier for the custodian signified by that record.

(ii)A field contained within a transactionDataRecord specifying the custodian at which the transaction signified by the record will settle and corresponding to the "custodianID" of a particular custodiansDataRecord.

A dialog box accessible via the "Add Custodian" selection on the tradeConfirmationMenu|input menu, which allows the user to create a new custodiansDataRecord. The following data may be input:

A measure of the issuer's ability to meet the terms of the investment by paying interest or dividends in the agreed manner, as well a repaying the principal of the investment at maturity. These ratings are issued by credit rating agencies (for a fee paid by the issuer) and are explicitly not investment recommendations in the buy/sell/hold sense. Most institutional fixed-income investors will not hold issues without a credit rating.

This is the yield reported in newspaper listings. It is simply the annual dividends payable divided by the current price of the security. See also currentYieldBid-spot. Sometimes referred to as runningYield.

The "curveAskPrice" is the price derived by computing the net present value of the cash flows in the curveAskTable according to a supplied yield curve.

One will note that the derivation of these option values is somewhat circular - the initial approximation is made with the prior day's yield curve, if available, or with a flat yield curve with a level equal to the mean average of the costBidYield of all instruments in the analytical universe if necessary.

The "curveBidPrice" is the price derived by computing the net present value of the cash flows in the curveBidTable according to a supplied yield curve.

One will note that the derivation of these option values is somewhat circular - the initial approximation is made with the prior day's yield curve, if available, or with a flat yield curve with a level equal to the mean average of the costBidYield of all instruments in the analytical universe if necessary.

The "curveMeanPrice" is the mean average of the curveBidPrice and the curveAskPrice. It may be computed with the discounting applied according to any particular curve.

It is used extensively in the calculation of curveVariance.

The "curve variance" is a measure used of the ability of the yield curve to account for the cash flows of all the instruments under consideration. It is this value which HIMIPref™ seeks to minimize during the calculation of the yield curve.

The "curve variance" for each instrument included in the calculation is summed to arrive at the total. First, the curveMeanPrice for the instrument under the curve is calculated.

A damping factor is applied during the calculation of an exponential moving average. It is a measure of the degree to which new data dominates the calculation. A damping factor of 1 means that only the first (earliest) measurement of any series is included in a calculation - a damping factor of 0 means that only the last (latest) measurement will be included.

Portfolios may be evaluated according to data from the transactions table (if "dataSourceTransactions" is true) or the holdings table (if false) according to choice.

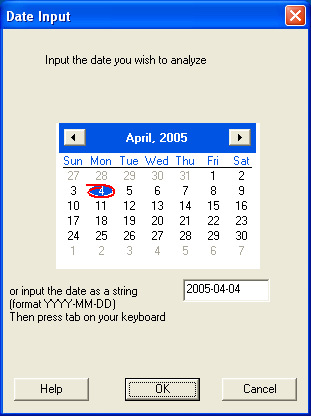

An input box allowing selection of a date. Either the desired date on the Calendar Control may be highlighted by clicking it, or the full date (in YYYY-MM-DD format) may be entered in the appropriate edit box. Note that there will usually be a restriction on the valid dates that may be entered - an error message will appear if an invalid date is chosen and the user may retry.

Also, note that the date is not actually chosen until the "OK" button is clicked; dates entered as text will be displayed on the calendar allowing for selection of a particular day of the week or month-end.

(i) The Dominion Bond Rating Service (DBRS) is a credit rating agency: it receives a fee from issuers to assign credit ratings to their borrowings, which often comprise commercial paper, preferred shares and bonds. Although there is clearly a potential for a harmful conflict of interest, the demand by investors (including Hymas Investment Management) for such credit ratings makes obtaining them virtually obligatory for the issuers. Further information regarding DBRS and updated rating information on issuers, may be obtained from their website.

(ii) A field contained within a creditRatingDataRecord, specifying the "DBRS" rating for the defined security and period. This datum is available through the creditRatingHistoryBox.

A dialog box accessible via the tradeConfirmationMenu|Input menu which allows for the input or edition of a dealerRecordType. The following fields are input by typing in the appropriate boxes:

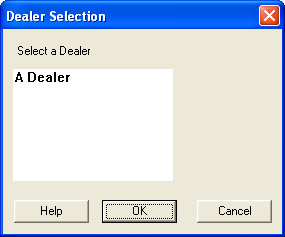

A dialog box utilized during the tradeInputProcess to allow selection of the counterparty to the trade. To select a dealer, highlight the dealerName of the dealer and click "OK"

When an issue is redeemed or retracted at a price above its par value, the difference between the two numbers is considered to be a "deemed dividend" and is taxed as a dividend.

Rarely issued, a "deferredPreferred" will not pay regular cash dividends for all or most of its life; the investor will receive his 'time value of money' in the form of a maturity price greatly in excess of the issuePrice.

The first date on which a listed issue has no closing quotation available on the Exchange. Issues which have been delisted are no longer traded on the Exchange - this usually happens due to reorganizations, such as redemptions. The database requires that all delistings be associated with an event recorded in the reorganization database, which provides information on what has happened to the issue. By convention, the value date of the reorganization database is equal to the delisting date.

(i) A field in a systemConstantsRecord that provides a short (not more than 50 characters) description of the record, indicating the type of portfolio for which the optimizableParameters have been optimized.

If the parValue of the instrument is less than the curveBidPrice, "differenceFromPar" is the difference between the two values; otherwise

If the parValue of the instrument is greater than the curveAskPrice, "differenceFromPar" is the difference between the two values, otherwise

"differenceFromPar" defaults to zero.

. In other words, "differenceFromPar" may be thought of as the change required in the parValue in order to get it within the bounds of curveAskPrice and curveBidPrice.

The amount by which the price under consideration (market price, redemption price, etc.) is under the issue price. An instrument issued at $25 and trading at $24 has a discount of $1. The opposite of "discount" is premium.

where blendedRate is the interest rate applicable according to the yield curve and the time to maturity and time is the time from the calculation date until the cashFlowDate

Note that if "blendedRate" is a constant, it may be referred to as the discountingRate.

A payment made to holders of shares in a corporation, paid from the profits of the corporation. Dividends on preferred shares are normally set in advance or calculated in accordance with a set formula, as stated in the prospectus. Unlike interest income, dividends are eligible for the dividend tax credit.

This parameter seeks to quantify the extra return that may be gained by capturing a dividend. If quotations of instruments were constant irrespective of dividend ex-dates, one would expect "dividendCapture" to be high - if flatBidPrice & flatAskPrice were constant, one would expect "dividendCapture" to be low.

A field in an instrumentDataRecord which specifies the number of dividend payments which are expected annually (virtually always either four or twelve).

The time between two successive dividends, assuming that dividends are paid in accordance with the terms of the prospectus. The interval can be measured between ex-dates, record dates or pay-dates according to need and context. The precise value of a "dividend interval" can vary from period to period, due to complexities of the calendar and, to a certain extent, the whim of the directors who declare the dividend.

A temporary variable calculated and stored during simulations to record dividends during the period between the ex-date and the record date. While such funds cannot be spent, not having been received, they are included as part of the portfolioCashValue. This value is reported by the portfolioReportBox.

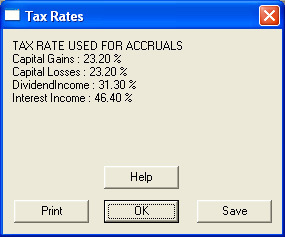

A method of treating dividend income under Canadian Tax Law, whereby a greater-than-actual amount of taxable income must be declared on individual tax returns, but a relatively large credit is deducted from actual tax owing. The effect is to reduce the marginal tax rate payable on dividends, which in the 2003 tax year is less than that on ordinary income, but greater than that on capital gains.

A calculated value used in the subsequent calculation of capitalGainFrictionBid / capitalGainFrictionAsk that seeks to quantify the sensititivity of the valuation to relatively small price changes. It is defined as:

A procedure called by calculateTradeSize which determines whether the instrument is eligible for purchase according to the systemConstantsRecord applicable to the trade.

The pseudoModifiedDurationCost of the issue purchased is examined. If it is undefined, the size of the trade is set to 0.

The numerical result of the eligibleForPurchase function. If the result is reported as "No Sol.", the instrument has passed all the tests set in that function. Otherwise, the value reported is the "Numeric Value" specified under the heading tradeSizeCalculationNotes if this value is noted as being so reportable.

A procedure called during the calculation of trade size.

If the size of either the sell side or the buy side of the trade has been reduced to zero (by the action of other trade size procedures called by calculateTradeSize) the entire trade is reduced to zero. This ensures that the valuation of an instrument is not used to determine the tradeScore or tradeDesirability of a trade which actually being performed against cash.

A hurdle rate is set equal to one-half the value of PARAMETER_PORTFOLIO_MINWEIGHT for each side of the trade that is defined (so a swap has the full value of this parameter, whereas an outright purchase or sale has only half the value). If the hurdle value is greater than trade weight, the size of the trade is set to zero.

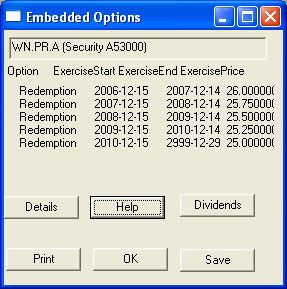

"Embedded Options" are options exercisable by the issuer or by the shareholder in accordance with the terms of the prospectus. These will most often be options to redeem or to retract the security.

They are referred to as "embedded" because they are intrinsic to the security and cannot be traded separately.

A text file stored in the userDirectory that logs error messages and other information specified by the HIMIPref™ client programme. This file is erased and re-written every time the HIMIPref™ programme is run. The administrator may ask, in the event of an error, for a copy of the "errorOutput.txt" file to be emailed to him.

The cut off date for determining whether a particular transaction is included in the accounting for the activePortfolio, which may be done on a tradeDate or valueDate basis.

the absolute value of the difference between the rewardComponentsBid (of the instrument sold) less the rewardComponentsAsk (of the instrument bought) is greater than the "hurdle", AND

this difference is negative

, then

both the difference and the "hurdle" are subtracted from "excessRewardDecreases"

Note from the definition that this value is constrained to be positive.

If either side of the trade is "Cash", then both excessRewardIncreases and excessRewardDecreases are defined as zero and therefore "excessRewardDifferenceValuation" will be zero.

The purpose of this component of bidToOfferPickup / offerToBidPickup is to account for situations in which unusual circumstances conspire to make a trade excessively attractive due to the influence of a single rewardComponentBid / rewardComponentAsk; the influence of this attribute, in essence, demands confirmation from several components and as such may be thought of as being related to rewardDecreasesValuation.

the absolute value of the difference between the rewardComponentsBid (of the instrument sold) less the rewardComponentsAsk (of the instrument bought) is greater than the "hurdle", AND

this difference is positive

, then

difference less the "hurdle" is added to "excessRewardIncreases"

Note from the definition that this value is constrained to be positive.

The first day of trading on which a buyer of shares is not entitled to receive the contemporary dividend (i.e. the shares are ex-Dividend commencing with the "ex-Date"). This date is therefore very important in the valuation of preferred shares and preferred securities.

"Without the Dividend.", i.e., the entitlement to dividend being referred to has been separated from the ownership of the shares. The opposite of "ex-Dividend" is cum-Dividend. See ex-date.

The date the holder of an option exercises his rights to effect the transaction specified in the terms of the option. In the reorg database, this date is referred to as the valueDate.

"issuance(isCall)" is issuance cost for calls, zero for puts

Note that the sum of the "exercise probabilities" of the elements of the list is constrained to be 100%, with any adjustment necessary performed against the latest, final maturity, element of the list.

"expected bid" = currentBid + amountAmortized * (termToCalculation/termToMaturity)^PRICE_AMORTIZATION_EXPONENT where "currentBid&quit; is the actual bid price of the instrument on the calculation date, "amountAmortized" is the maturity price less the "current bid" "termToCalculation" is the term, in years, from the calculation date to the exerciseDate "termToMaturity" is the term, in years, from the calculation date to the ultimateMaturityDateUsed

An exponential moving average takes all information in the given period into account, assigning greater weight to more recent data: each day's data is applied successively to the moving average, so that:

EMA(new) = DF*EMA(old) + (1 - DF)*data

where

EMA(new) is the new exponential moving average

EMA(old) is the prior day's exponential moving average

In certain cases, the analytical methodology may adjust the damping factor and the data depending upon the relationship between the data and EMA(old). See volume - average.

The completion of an order. An investor who put in an order to buy 200 shares and actually bought 200 shares has been filled; if he actually bought only 100 shares, he has been partially filled; if no shares were purchased he has not been filled.

This is the dividend that is paid upon the maturity of an instrument. It may be more or less than a regular dividend payment, depending upon the relationship between the maturityDate and the prior dividendpayDate.

Each completed calculation of an option calculation list will include exactly one element with its maturity flag set to indicate the fact that it is considered a "final maturity" with no calculations being performed after the exercise date of the element.

The maturity flag of a "final maturity" may take one of four values:

The yieldToMaturity for a costBidDiscountingTable is performed using a formula to derive the present value of regular dividends and the maturityPrice, to which is added the present value of any adjustments. The first dividend paid on an instrument after its issue is usually not the regular amount - it may be more or less than the regular amount depending upon the relationship between the issue date and the first dividend payDate. This difference is entered on the adjustment table so that the first dividend, in sum, is properly accounted for.

An issue which commences its existence paying a fixed dividend, but which changes to floating rate on some particular date in accordance with the prospectus, e.g., The Maritime Life Assurance Company Non-Cumulative Redeemable Second Preferred Shares, Series 1:

The initial dividend, if declared, will be payable on December 31, 1999 in the amount of $0.17405 per share, based upon an anticipated issue date of November 19, 1999. After December 31, 2004, dividends will be at the Applicable Rate in effect from time to time. The "Applicable Rate" for any quarterly dividend period during each five year period commencing after December 31, 2004 will be determined by applying to $25.00 one quarter of the greater of (i) 90% of the Prime Rate and (ii) 5.85%.

An asset class including bonds and most preferred shares, comprised of all instruments in which the expected cash flows are an obligation of the issuer that is known in advance (or, in the case of floatingRate issues, is calculated from a market rate independent of the fortunes of the issuer via a set formula). This asset class is distinguished from equity by this prior arrangement, which is described in the prospectus - most simply stated, a "fixed income" investor will receive fixed amount, while an equity investor will pay or receive the difference.

An issue which commences its existence paying a fixed dividend, but which changes this rate on some particular date or dates in the future in accordance with the prospectus. For example, the BCE Inc. prospectus dated December 10, 1997 for the issue of "Cumulative Redeemable First Preferred Shares, Series Y" included the following provisions in the section "Principal characteristics of Series Z Preferred Shares"

Dividends: Fixed cumulative preferred cash dividends payable quarterly on the first day of March, June, September and December in each year.

At least 45 days and not more than 60 days prior to the start of the initial dividend period beginning on December 1, 2002, and at least 45 days and not more than 60 days prior to the first day of each subsequent dividend period (the initial five year dividend period and all subsequent five year dividend periods being referred to as a "Fixed Dividend Rate Period"), BCE Inc. shall set, and provide written notice of, a Selected Percentage Rate for the ensuing Fixed Dividend Rate Period. Such Selected Percentage Rate shall not be less than 80% of the Government of Canada Yield determined on the 21st day preceding the first day of the applicable Fixed Dividend Rate Period.

This value is useful as an indicator of market price which is not subject to the "sawtooth" pattern expected of most intruments, which should be subject to a decrease in price on every ex-date approximately equal to the dividend payable. This value is also referred to as flatAskPrice-Spot.

A calculated value of the price of each instrument, adjusted to eliminate the effect of so-called accrued dividends. The "Current Bid (Flat Value)" is then the actual bid price less the accrued dividendFlatValue

This value is useful as an indicator of market price which is not subject to the "sawtooth" pattern expected of most intruments, which should be subject to a decrease in price on every ex-date approximately equal to the dividend payable. This value is also referred to as flatBidPrice-Spot.

An issue is referred to as being floating rate if the amount of dividends or interest income payable to the holders is dependant upon a short-term rate in a manner defined in the prospectus. This short-term rate is usually, but not always, the Canada Prime Rate; the formula used to determine the rate payable on the issue can often be quite complicated. Whether or not an issue is floating rate is considered to be a risk attribute. Note that in HIMIPref™ an issue is considered to be floating-rate for risk determination purposes even if it is currently fixed-rate, but will become floating rate on a definite date in the future (a fixed-floater). Issues are not considered to be "floating rate" if the dependence upon the floatingRateIndex is currently constrained by a cap or collar on such rate. For example, the prospectus for NA.PR.J (National Bank Non-cumulative First Preferred Shares Series 13) dated July 3, 2000 states:

After August 15, 2005, the dividend on the Preferred Shares Series 13 for each quarter will be determined by multiplying $25.00 by one quarter of the greater of (i) 95% of the rate which is the average of the Prime Rate in effect each day during the three months ending on the fifteenth day of the month immediately preceding the month in which the dividend payment date occurs and (ii) 6.15%

This is reflected in HIMIPref™ as formulaFLOATING_RATE_GO2126. When the canadaPrimefloatingRateIndex falls below about 6.47%, the dividends will not fall proportionately, and therefore the issue is not be considered to be "floating rate" when this is the case.

This field specifies the formula to be used in computing the instrument's floatingRate from the supplied value of the floatingRateIndex, subject to adjustments indicated by the fields formulaMax and formulaMin.

Friction is used to denote the costs of a performing a trade. These costs include dealers commissions, settlement fees and capital gains taxes. Of these, the first two will always work against a decision to trade, as they always work against the investor. Capital gains taxes may work in the investor's favour if the instrument to be sold is trading at a loss and the investor currently has a taxable capital gain - in this case, the fact that performing the trade will reduce the amount of tax already payable will work in favour of a decision to trade.

For example, consider the case of an investor who owns 1000 shares of TRP.PR.X, bought at $45 and currently trading at $44. These shares are virtually identical to TRP.PR.Y. The investor has (through other investments) a taxable capital gain of $1000, on which tax will be paid at a rate of 32.9%, or $329. If the investor sells TRP.PR.X to buy TRP.PR.Y at the same price, then his portfolio will, in terms of expected future returns, be almost unchanged by the trade, but the fact that a $1000 capital loss was realized will eliminate his current capital gain and reduce his tax by $329.

There is no free lunch: when the TRP.PR.Y are sold later on, the capital gain will be greater by the same $1000 and taxes will be correspondingly greater. Transaction costs also must be considered. However, the fact that these taxes will be payable further into the future than would otherwise be the case (in many ways equivalent to an interest-free loan from the tax-man) increases the attractiveness of the trade.

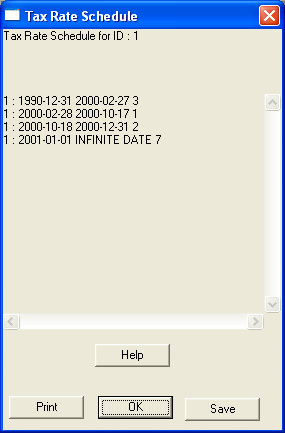

(i) A field contained in a taxRateScheduleRecord. Its purpose is to define the starting date (inclusive) of the period for which the record is effective in identifying a taxRateDataRecord to be used for analytical purposes. This datum may be displayed in the taxRateScheduleBox.

(ii) A field contained in a FRBenchmarkType record. It specifies the starting date (inclusive) of the period for which the record is effective in recording the benchmark interest rate. This datum is available in the ratchetRateCalculationBox.

A calculated or defined variable that quantifies some aspect of an instruments characteristics without making a judgment on the importance of that characteristic. Most "fundamentalAttributes" are operated on by optimizableParameters in order to determine the rewardComponentsBid / rewardComponentsAsk of that instrument; other "fundamentalAttributes" are used at various stages in the calculation of tradeScore and tradeDesirability to assess the degree of confidence that should be placed in the relative valuation of the securities considered.

Calculated "fundamentalAttributes" are stored in the system in the riskRewardDataType structure.

A function called during the calculation of Dividend Amount (Flat Value), among other places. It calculates the amount of a single dividend payment for a single instrument by determining, in order:

A context menu available on the graphDocument that can be used to provide further information regarding the data plotted on a graph. Specific versions of this menu are:

A context menu available on the graphDocument when right-clicking on a point produced on a graph created through the "Instrument Price Variance" or "Attributes" selection on the graphMenu|Settings popup menu. Most selections from this menu allow the choice of dialog boxes which will provide further details of the calculations performed on the instrument/price represented by that point. Specific choices are:

Remove Point from Graph : The right-clicked point will no longer be drawn on the graph. Grid lines may be recalculated (see graphMenu|View) and the point will not be included as part of a regression analysis (see regressionResultBox

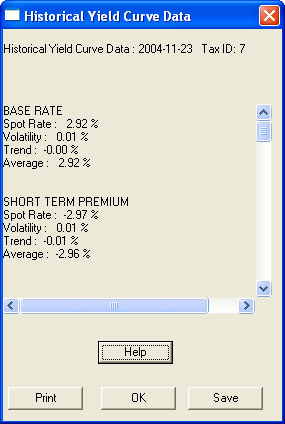

A context menu displayed when a point on a graph of historical yield curve data ("Select Period (Yield Curve Data)" on the graphMenu|settings menu) is right-clicked.

This context menu is available via the "Data Selection | Select Specific Data" selection on the graphMenu after "Attributes" has been selected on the graphMenu|Settings menu.

It allows for the choice of data to be displayed:

"Select X-axis" : displays the fieldsMenu to select the X-Axis

"Select Y-axis" displays the fieldsMenu to select the Y-Axis

A pop-up menu accessible via the "Data Selection|Select Specific Data" selection on the graphMenu after "Select Period (Yield Curve Data)" has been selected on the graphMenu|Settings menu.

This pop-up menu allows the choice of what yieldCurve data as recorded on the yieldCurveAveragesRecords is to be graphed for the defined period:

A dialog box accessible via the "Show Data" selection on "graphMenu|Reports" menu.

This dialog reports the data displayed on the graph; the upper panel displays the title and sub-title of the graph, followed by the captions of the "X" and "Y" axes. The middle panel displays the data, with each line representing one point on the graph, specifying the graphSetType, the "X" value and the "Y" value. Finally, the lower panel allows selection of how the data in the middle panel are to be sorted - options are

A document allowing the preparation of graphs, accessible via the "Graphs" selection on the mainMenu|Research popup menu. The "graphDocument" is controlled by the graphMenu and additional reports and actions are available through the graphContextMenu.

To prepare a graph, the type of data to be plotted is first selected from the graphMenu|Settings popup menu, and then the specific data selected via the graphMenu|DataSelection|"Select Specific Data" selection.

"Select Specific Data" : Displays a context menu dependent upon the choice made under graphMenu|Settings

Instrument Price Variance : displays the fieldsMenu for selection of the Y-axis of the graph. Right-clicking points on the graph produced will display the graphContextMenu|attributes context menu.

Comparator : These menu items will only be available if "Select Historical Instrument" has been selected on the graphMenu|Settings menu.

Set Comparator : This will allow selection of another instrument from the instrumentSelectionBox and allow the plotting of data for this instrument to be displayed on the graph together with that of the "main" instrument

Delete Comparator : deletes comparator information from the graph.

A popup accessible via the "Settings" selection on the graphMenu which allows selection of the type of data that is to be displayed on the graphDocument. Options available are:

Instrument Price Variance : displays the instrumentSelectionBox followed by the doubleInputBox for selection of the price range. This selection allows for a determination of how an instrument attribute (selected via the standard fieldsMenu) will vary with its price and enables the "Change Price Range" selection on the graphMenu|View popup menu.

Select Period (Yield Curve Data) : This selection graphs yieldCurve coefficients vs. time. The dateInputBox is displayed twice to select the period, then the taxRateQueryProcess is run and finally the graphContextMenu|yieldCurveTypeSelect context menu is displayed to select the field of the yieldCurveAveragesRecord that is to be graphed. Multiple series may be displayed via the "Data Selection|Select Specific Data" selection of the graphMenu

Attributes : Allows the graphing of two selected attributes against each other for data calculated on a given date. The dateInputBox is displayed to select the date, then the taxRateQueryProcess is run, then the booleanInputBox is displayed to determine whether the points displayed should be restricted to instruments eligibleForPurchase. This choice enables the "Segregate by Credit", "Credit Class 1", "Credit Class 2" and "Credit Class 3" selections on the graphMenu|View popup menu.

Segregate By Credit : Enabled only when "Attributes" has been selected on the graphMenu|Settings menu. When selected, points representing instruments of different creditClasses will be represented by boxes of different colours.

Credit Class One : Enabled only when "Attributes" has been selected on the graphMenu|Settings menu. When selected, points representing creditClass1 will be displayed.

Credit Class Two : Enabled only when "Attributes" has been selected on the graphMenu|Settings menu. When selected, points representing creditClass2 will be displayed.

Credit Class 3 : Enabled only when "Attributes" has been selected on the graphMenu|Settings menu. When selected, points representing creditClass3 will be displayed.

Regression : Performs a multilinear regression of the data displayed on screen and displays the results in a regressionResultBox

Change Price Range : Enabled only when "Instrument Price Variance" has been selected on the graphMenu|Settings. This will display the doubleInputBox for selection of a price range over which the selected instrument should be varied as a proportion of its market price.

A setting of graphSetType that indicates the data is supplied as a comparator for the main data referred to with the indicator GRAPH_SET_MAIN. It may be used when plotting the yieldCurve for a single day (graphMenu|Settings|Yield Curve) and for the first instrument selected when plotting historical attribute data (graphMenu|Settings|Historical Instrument). This set will be indicated on reports as "Comparator Set - 1".

A setting of graphSetType that indicates the data is supplied as a comparator for the main data referred to with the indicator GRAPH_SET_MAIN and is distinct from that identified with GRAPH_SET_COMPARATOR. It may be used when plotting the yieldCurve for a single day (graphMenu|Settings|Yield Curve). This set will be indicated on reports as "Comparator Set - 2".

A setting of graphSetType that indicates the data has been created by determining the difference in the "y"-values between the GRAPH_SET_MAIN and GRAPH_SET_COMPARATOR points for a given value of "x".

A setting of graphSetType that indicates the data is the "anchor" for the graph. It is used when plotting the yieldCurve for a single day (graphMenu|Settings|Yield Curve) and for the first instrument selected when plotting historical attribute data (graphMenu|Settings|Historical Instrument). This set will be indicated on reports as "Main Set".

An enumerated type used in the determination of which points on the graph are related. Each point displayed on the graphDocument is associated with one of the following possible values:

The ability of the investor to demand cash from the issuing company in exchange for his shares. The amount of cash, notice period and time at which this right may be excercised being specified in the prospectus at time of issue.

A methodology, displayed in the riskPerformanceBox, of analyzing the universe of preferred shares examined by HIMIPref™ whereby for each binary riskAttribute (as well as liquidityMeasured and Credit Class UNRATED) the universe is sorted into two subsets, such that each subset is homogeneous for the attribute examined. A determination is then made of the distribution of the other binary indicators in each subset. Note that in a perfectly homogeneous universe, the analyses of the two subsets would yield identical results.

Results are reported as a series of columns, each "major" column reflecting the attribute used to make the division between the two subsets, which are the "minor" columns labeled "True" and "False" below the major column heading. Rows are reported in the same order from top to bottom as the columns are presented from left to right.

Example: Consider the following extract from the table of a Raw Heterogeniety Analysis:

Retractible

Split Share Corp

True

False

True

False

71-0

0-70

32-0

39-70

32-39

0-70

32-0

0-109

From the top row of the first major column, we obtain the trivial (reflexive) result that of 71 Retractible issues examined, 71 were retractible and 0 were not. A similarly trivial result is obtained for "Split Share Corp" in the second row of the second major column.

More interesting results are obtained off the diagonal. From the second row of the first major column, we learn that of the 71 retractible issues, 32 were Split Share Corporations and 39 were not. Of the 70 non-retractible issues, none were Split Share Corporations.

In a Percentage Heterogeniety Analysis the data are presented as a percentage of the cell that is "True", so the 32-39 split in the above table is reported as 32 / (32+39) = 45.07%.

This selection graphs a selected attribute of a particular instrument (Y-axis) vs. time (X-axis); it is accessible via the "Historical Instrument" selection on the graphMenu|Settings popup menu on the graphDocument.

Some data normally accessible on the fieldsMenu may not be plotted with this option, as these data are not stored subsequent to their calculation and immediate display:

where "historicalVolatility[x]" is the historical volatility on day x dailyVolatility is { 0, if the day's change is the same sign as the historicalTrend; or adjustedSpotRate[i] - spotValue[i-1], otherwise}

If there is no record for the prior day, the "historicalVolatility" is set to 0 if the spotValue is defined, otherwise it is also undefined.

The ask price of the shares as defined in the activePortfolio. This may not be equal to the ask shown elsewhere on the reportSummary since the holdings may have been valued as of a different date.

The bid price of the shares as defined in the activePortfolio. This may not be equal to the bid shown elsewhere on the reportSummary since the holdings may have been valued as of a different date.

This component seeks to quantify the degree by which valuations should be reduced solely due to a desire to avoid maximizing holdings in an issue before the best time - that is, to retain a capacity to purchase additional shares of an attractive issue should the price decline further. This penalty is applicable only to the valuation of the issue to be purchased. It is equal to:

A calculated vector of RISK_MEASUREMENT_AXIS_TYPE_MEMBERS length, one for each risk attribute. For each member, if the corresponding values of portfolioWeightedRisk and indexWeightedRisk are both defined, the "holdingsRiskDifference" is obtained by subtracting the latter from the former; or else the value will be set equal to the corresponding value of the attribute for the instrument being sold; or if no instrument is being sold, the value will be set to "undefined"

The "holdingsRiskDifference" vector is used in the calculation of riskUp, riskDown and subsequently riskDistance.

A temporary variable calculated and stored during simulations to record the taxes which will become payable on the next tax payment date. Such amounts have not yet affected the cash in the portfolio, but are allowed for as part of the portfolio cash value.

A collection of issues with assigned weights which purports to provide an overall view of the market or a specified subsection thereof. The most important index for Canadian preferred share management is the BMO Nesbitt Burns 50 Index.

The index is used when optimizing portfolios according to the portfolio method in order to determine the risk characteristics of the portfolio and the effect of any proposed trade.

The index used in portfolio management is a constraint

(i) A field in an indexCompositionRecord which specifies the index to which the information in the record applies. It corresponds to the "indexID" field in an indexNamesType record.

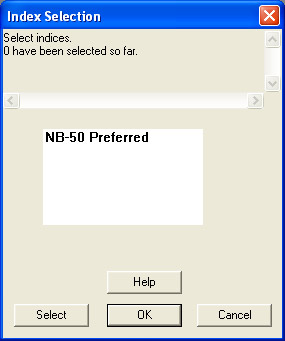

An input box allowing the selection of one or more indices from the defined list. The text in the selection box is the indexName field of indexNamesType.

To select an index, highlight the indexName and click the "Select" button; the number of indices selected and their names will then be listed in the upper panel of the "indexSelectionBox". When all desired indices have been selected, click the "OK" button to accept the list.

The particular risk attribute for each security in the portfolio is incalculable.

If a particular risk attribute for a particular security is incalculable, the "indexWeightedRisk" is calculated as if that value was equal to the average of the other values.

A market is inefficient if information regarding the value of a particular investment is not communicated rapidly to its market price. If, for example, a listed company existed which had as its sole business the holding of particular common shares for investment purposes, we would expect changes in the prices of those shares to be instantaneously reflected in the price of the holding company's shares. The market is "inefficient" to the extent that this effect is delayed, or not reflected at all.

Another example would be two series of bonds issued by the same company, which had identical terms, issue sizes and distribution of holders. The market would be inefficient to the extent that the prices of these bonds on the market was not identical.

A procedure called as part of the determination of trade size, which performs a number of steps to determine a rough approximation of the size of trade being contemplated. In the portfolio method and in the issue method when numberSwapSecuritiesDesired is non-zero:

Desired cash proceeds from the sale are estimated as the cash requirements for the purchase, less cash already in the portfolio.

This is adjusted to reflect a sale in board lots which does not exceed current holdings of the issue sold.

If such a sale would leave less than PARAMETER_PORTFOLIO_MINWEIGHT weight of the issue sold in the portfolio, the entire holding of the issue is set to be sold.

The number of shares to be purchased is then calculated to reflect an integral number of board lots with a total value less than the available cash.

Note that "instrument reversion parameters" may be either positive or negative: a negative value implies that reversion-to-mean is the operative principle, while a positive value implies that momentum is more important.

Note that "instrument valuation parameters" is constrained to be positive: all the relevent calculated values are considered to be "good" for the instrument - e.g. higher yield, higher priceDisparity, etc.

A table contained within the permanentDatabase that contains instrumentDataRecords. It contains basic information regarding all instruments that have ever been examined by HIMIPref™.

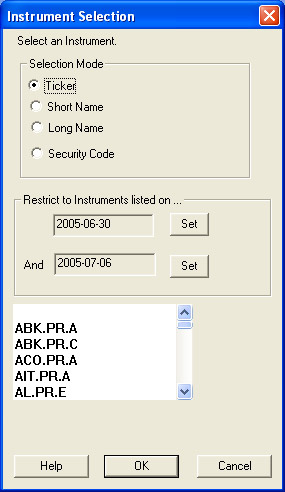

A dialog box in which a single instrument may be selected from a list of those available. As defined by the radio buttons on the box, the list may be presented as one of:

Through application of this scaling factor in the calculation of totalRewardBid / totalRewardAsk (specifically, classRewardYieldBid / classRewardYieldAsk), the end-value of these calculated variables is expected to be identical no matter what multiplier is applied to the parameters (which aids in simulation) and these values should reflect the expected percentage return over one year.

Interest income is paid by the issuer on preferred securities, sometimes referred to as COPrS's, from its pre-tax income. Such income, unlike dividends does not have the benefit of the dividend tax credit and is taxed at the marginal rate associated with ordinary income.

Information regarding the type of income paid by a security is contained in the instrumentDataRecord. This is one of the riskAttributes of HIMIPref™.

This is the fraction of the issue price that an issuer may expect to pay as sales commission on a new issue of shares. It is constrained to be between 0.0 and 0.1.

This penalty is applied to each instrument in accordance with the number of multiples of effectiveMinWeight that are held in the portfolio. The objective behind this parameter is to make it harder to increase a position as the existing position becomes a greater part of the total portfolio, so that it is harder to buy the nth minWeight block of any given instrument as n increases.

The value of this parameter is constrained to be non-negative.

A method of portfolio optimization in which the possible individual sales are paired with each each possible purchase and a decision regarding whether to trade or not is based solely on consideration of these two issues - the overall portfolio and its risk characteristics are not considered at all. Thus, a portfolio optimized in accordance with the "issue method" may, for instance, be holding only floating rate issues.

A trade is indicated if the following conditions are met:

Implementation of the "issue method" is affected by the value of the portfolio data record setting for desired swap issues - a non-zero constraint may be relaxed to allow such a portfolio to hold at least one issue affected by the constraint.

The price at which the instrument was issued, that is, sold to investors directly by the company. This is the primary market for the shares; subsequent trading between investors is referred to as the secondary market. The issue price is normally equal to the par value of the shares; the few exceptions to this rule are usually deferred preferred shares.

The issuers are the companies who sell their stock on the primary market and receive the issue price from investors in return for agreeing to meet the obligations set forth in the prospectus. Their ability to meet these continuing obligations is estimated and quantified through their credit rating.

An order to execute a trade only at a certain price or better. This may result in obtaining only a partial fill or perhaps not executing the trade at all.

The ability to trade in an investment without affecting the market price. It may be possible, for instance, to buy 100 shares of Royal Bank at $50 instantly, but a large investor seeking to buy 100,000 shares immediately might have to pay $51 in order to have his order filled. If the larger investor had put in a limit order for 100,000 shares at $50, he might end the day with a fill of fewer shares, if any, than he wanted to buy.

See maxDaysToTrade and swap value for commentary on the application of this concept to HIMIPref™.

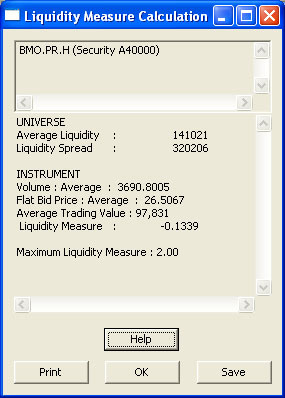

A measure of the relative liquidity of the issues available for investment. This value is computed for each instrument when the values for liquidityAverage and liquidityStandardDeviation are known and is equal to:

This value is used in the computation of the yieldCurve in which, like a risk attribute, there is the possibility of the instrument's curvePrice being dependent upon the value of this attribue.

The first date the issue is traded on the exchange (see listing) and has a closing quotation available. The "listingDate" of an instrument is recorded in its instrumentDataRecord.

"Long" is usually an adjective denoting ownership. Thus, if you own 100 shares of something, you are said to be "long" 100 shares. The word can also be used as a noun (e.g. "The longs expect interest rates to fall") and a verb (e.g. "We should be longing retractibles").

The long name of an issue is a 50-character representation of the legal name of the issue. The long names used in HIMIPref™ will generally, but not always, be the same as those reported by the Toronto Stock Exchange. These "long names" are recorded as an eponymous field in an instrumentDataRecord. See also short name.

A calculated value, used in the subsequent calculation of totalBuyCommission and applicable only when PARAMETER_TRADING_MAXDAYS is aggressively set to a value in excess of 1.0.

As stated by Robert W. Kopprasch, Ph.D., CFA, in The Handbook of Fixed Income Securities, Second Edition, Dow Jones-Irwin, 1987, ISBN 0-87094-745-1, referencing Frederick Macaulay, Some Theoretical Problems Suggested by Movements of Interest Rates, Bond Yields and Stock Prices in the United States since 1856, National Bureau of Economic Research, 1938,

...described a measure he called duration, which measures the weighted average time until cash flow payment. The weights are the present values of the cash flows themselves

so

"Macaulay Duration" = sum(w[i] * t[i]) / sum(w[i]

wherew[i] is the present value of the i'th cash flow, which becomes due at time t[i].

"Macaulay Duration" is a useful approximation of sensitivity to interest rates, but can give very misleading results when the yield curve changes shape. It is often used in the calculation of modified duration.

Note that the numerator in the equation above, sum(w[i] * t[i]), may be referred to as totalDollarDuration, while the denominator is presentValue.

A popup menu accessible through the mainMenu. This menu gives access to major file-changing commands in the system

Next Business Day : changes the analyticalDate to the next business day. If there is no priced date following the current analyticalDate, the system is reset so the final effect is no change.

A popup menu accessible via the "activePortfolio" selection on the mainMenu|reports popup menu. Data displayed via this menu reflect the settings and calculations of the activePortfolio